What Happens If You Cosign a Loan and the Other Person Doesn’t Pay?

Cosigning a loan can be a helpful way to assist a friend or family member in securing financing. But what happens if you cosign a loan and the other person doesn’t pay?

Failing to pay a cosigned loan on time harms both parties. The lender reports late payments to credit bureaus, lowering both credit scores. The cosigner must cover missed payments and may face collection actions or legal consequences. This can damage relationships and impact future loan approvals.

If you’ve been left on the hook for someone else’s loan, you still have legal options to protect your finances. Call Kostopoulos Bankruptcy Law at 877-969-7482 to speak with an experienced debt relief attorney. With decades of experience helping clients manage cosigned debt through negotiation, settlement, and bankruptcy solutions, we’ll help you minimize the damage and regain control of your financial future.

In this article, I’ll explain the risks, consequences, and steps you can take to protect yourself when a cosigned loan goes unpaid.

Your Rights, Options, and Legal Help in California

Worried about co-signing a loan? Discover what happens if the borrower defaults, your legal rights in California, and how a bankruptcy attorney can help.

Your friend asked you to co-sign their auto loan, and now they’re behind on payments. Panic sets in. You helped them get the car they needed, but now you’re in need for debt relief. If the borrower doesn’t pay, you might even be contacted by a debt collector. What happens if you co-sign a loan and the other person doesn’t pay? Understanding the legal consequences of co-signing is crucial.

This guide dives into the complex world of co-signing, exploring the risks, legal implications, and solutions available in California.

We’ll explore what happens if you cosign a loan and the other person doesn’t pay, focusing on the impact on your credit score, legal obligations, and financial health. We will also provide practical advice for protecting yourself and managing non-payment situations.

Whether you’re already a co-signer facing trouble or considering co-signing in the future, understanding your rights and options is crucial.

Understanding Co-Signing: A Deep Dive

Cosigning a loan can be a generous gesture, but it comes with significant responsibilities and risks. Before we delve into the potential problems, let’s clarify what co-signing means and the responsibilities it entails.

What Co-Signing Legally Means

Co-signing a loan is like offering yourself as a backup plan for the lender. Co-signing reduces the lender’s risk by providing them with an additional guarantor, ensuring they have another source of repayment if the primary borrower fails to make payments.

Imagine the primary borrower as the main performer in a show, and you, the co-signer, are the understudy, ready to step in if the main performer can’t continue. In the financial world, co-signing means you agree to be legally responsible for the loan if the main borrower fails to make payments.

When you cosign a loan, you are agreeing to be equally responsible for the loan payments if the primary borrower defaults. This means that any missed payments or defaults will affect your credit score and may lead to legal action. Cosigning can apply to various types of loans, including auto loans, personal loans, and credit card debt.

Why Do People Cosign Loans?

People often cosign loans to help a family member or friend who has a poor credit history and cannot qualify for a credit product on their own. This can be a way to support loved ones financially, but it also means taking on significant risk if the other party fails to make the payments.

Co-Signer Responsibilities and Legal Obligations

Co-signing doesn’t just mean lending your good credit; it means you’re taking on equal responsibility for the loan payments, including assuming debt responsibility alongside the primary borrower to avoid late fees and potential damage to your credit record.

As a cosigner, you have equal responsibility with the primary borrower for repaying the loan amount. If the borrower defaults, you are legally obligated to make the loan payments. This can include paying late fees and court costs if the matter goes to small claims court.

Missed payments by the main borrower will damage both your credit scores and potentially lead to a collection agency contacting you for the unpaid debt. Your financial decisions, including co-signing, are reported to the three major credit bureaus (Experian, Equifax, and TransUnion), impacting your credit report and credit rating.

Financial Implications for Cosigners

Cosigning a loan can have major implications for your financial health, including the serious financial implication of a loan default on the co-signer’s credit report. Missed payments by the borrower will appear on your credit report, potentially lowering your credit scores. This can affect your ability to secure new credit products or loans in the future.

Cosigning in California: State-Specific Considerations

In California, cosigners are subject to specific state laws that outline their legal responsibilities. It’s important to understand these laws to protect yourself and manage your obligations effectively.

The Different Types of Loans You Might Co-Sign For

Co-signing is common for various types of loans, including:

- Auto loans: Help someone purchase a vehicle.

- Personal loans: Cover various expenses like medical bills or home repairs.

- Student loans: Assist with educational costs.

- Small business loans: Help a friend or family member start a business.

- Mortgage loans: Support in acquiring a home.

The terms and implications of co-signing can vary slightly depending on the specific loan type and lender.

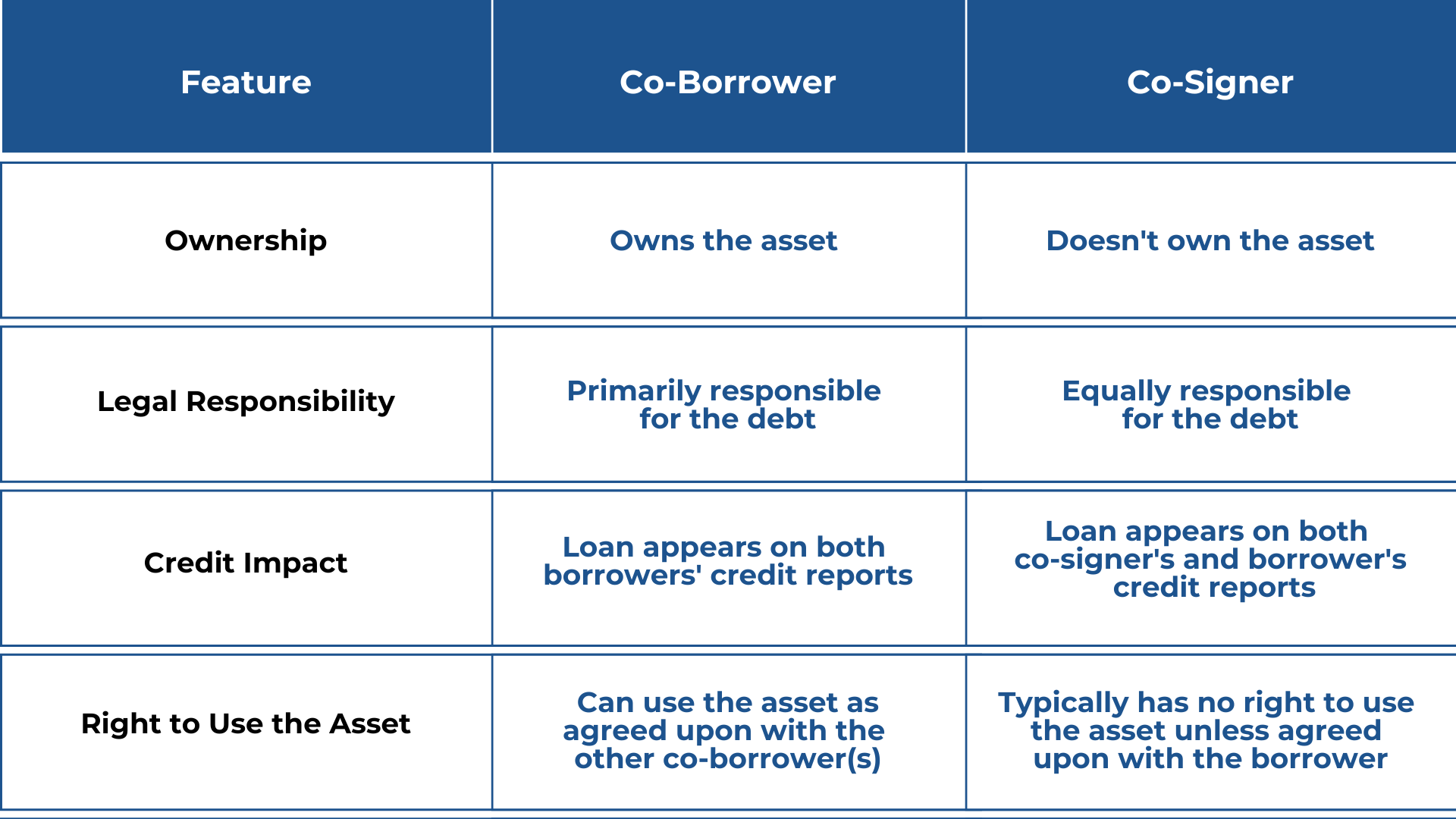

Co-Borrower vs. Co-Signer: What’s the Difference?

Many people confuse co-borrowers and co-signers. While both share responsibility for the loan, their rights and ownership differ:

Risks and Consequences of Cosigning

Impact on Credit Score

When the borrower misses a payment, it negatively affects your credit score. The missed payments will be recorded on your credit history, making it more challenging to secure future credit products or loans. Additionally, high credit utilization, especially when payments are missed, can significantly impact your credit scores, as it indicates a higher risk to lenders. Maintaining a good credit score is crucial for your financial future.

Potential for Legal Action

If the borrower defaults on the loan, the lender may take legal action against you to recover the debt. This can result in significant court costs and additional financial burdens. It’s essential to understand your legal responsibilities as a cosigner to mitigate these risks.

Emotional and Relational Strain

Cosigning a loan for a family member or friend can strain personal relationships if the borrower fails to meet their financial obligations. The stress and financial pressure of covering missed payments can lead to conflicts and emotional distress.

The Nightmare Scenario: When Borrowers Default

No one co-signs a loan expecting the borrower to default, but it’s a reality that many co-signers face. Let’s explore what happens when the unthinkable occurs. Default can lead to collateral damage if the loan is secured, impacting not just the borrower’s credit but also the co-signer’s financial stability.

What Happens to a Cosigner if the Borrower Defaults?

When the primary borrower misses payments or defaults, it’s not just their credit score that suffers; co-signers experience the same negative impact on their credit history, making it difficult to get a new loan or even rent an apartment.

The lender isn’t required to exhaust all options with the borrower before coming after you. As a co-signer, you might be their first target for recouping the loan depending on your financial health.

You could face:

- Collection calls and letters: Constant harassment from debt collectors.

- Lawsuits: The lender can sue you for the unpaid debt, leading to court costs and potential wage garnishment.

- Damaged credit: Late payments and defaults will significantly lower your credit score, making it harder to obtain future loans or credit.

Can a Co-Signer Take You to Court in California?

Yes, they can, if the co-signer ends up paying the debt. This is possible under California law, although co-signers typically try to resolve the issue amicably first. A co-signer who has paid the debt can take legal action, such as filing a lawsuit in small claims court to recover the money they paid, including any court costs. This is where a bankruptcy attorney can be invaluable, guiding you through the legal process and helping you understand your options.

Taking Action: Protecting Yourself as a Cosigner

While co-signing can be risky, there are steps you can take to protect yourself and minimize the potential consequences.

How to Avoid Loan Default as a Cosigner

- Open communication: Maintain regular communication with the primary borrower about their financial situation.

- Monitor payments: Regularly check loan statements and set up payment alerts to stay informed.

- Written agreement: Create a written agreement between yourself and the borrower outlining expectations and responsibilities.

- Financial education: Encourage the borrower to improve their financial literacy and budgeting skills.

Evaluating the Borrower’s Financial Situation

Before agreeing to cosign a loan, it’s crucial to evaluate the financial situation of the primary borrower. Ensure they have a stable bank account and the ability to make timely payments. Reviewing their credit history and financial health can help you make an informed decision.

Understanding the Loan Terms

Thoroughly review the loan agreement to understand the loan amount, monthly payments, and any clauses that may affect your credit scores if the borrower defaults. Pay attention to the terms and conditions, including any penalties for late payments.

Negotiating Cosigner Protections

Consider negotiating for a cosigner release clause that allows you to be removed from the loan agreement after a certain period of on-time payments by the primary borrower. This can reduce your long-term risk and protect your credit scores. Additionally, it’s crucial to discuss loan security measures, such as a cosigner release clause, to ensure the co-signer has an exit strategy, enhancing the security of the loan for both the borrower and the cosigner.

Dealing with Non-Payment

Immediate Steps to Take When Borrower Misses Payments

If the borrower misses a payment, contact them immediately to discuss their financial situation and find out why they are struggling to make the payments. Communicate with the lender to explore possible solutions, such as adjusting the payment schedule.

Steps to Take if You Can’t Make the Payments

If you’re struggling as a co-signer, consider refinancing the loan to remove the original borrower or explore cosigner rights options, but always consult with a legal professional for guidance. Other options include:

- Loan modification: Negotiate with the lender for modified terms, like a lower interest rate or extended repayment period.

- Ask for a Cosigner Release: In some cases, you might be able to request a cosigner release from the lender. This releases you from future liability for the loan. However, lenders are not obligated to grant this release, and it usually requires the borrower to demonstrate a consistent payment history and meet specific financial criteria.

- Debt consolidation: Combine multiple debts into a single loan with a potentially lower interest rate.

- Debt management plan: Work with a credit counseling agency to create a structured repayment plan.

- Exploring Refinancing Options: Refinancing the loan can help lower the monthly payments and make it easier for the borrower to stay current. This can prevent further damage to your credit scores and reduce the risk of legal action.

- Bankruptcy: This might be a last resort, but it can offer relief from overwhelming debt.

How to Take Possession of a Car You Cosigned For in California

If the borrower defaults on a car loan you co-signed, initiating asset recovery by taking possession of the vehicle in California might be within your rights. However, this is a complex process with legal implications.

Understanding Your Legal Rights

Your legal rights as a co-signer to repossess a car depend on the specific terms of the loan agreement and California law. Review the loan documents carefully to understand your rights and responsibilities.

Practical Steps to Take

If you decide to repossess the car, you’ll typically need to:

- Notify the borrower: Inform them in writing of your intention to repossess the vehicle.

- Obtain the keys: If possible, get the keys from the debtor voluntarily.

- Hire a repossession agency: If the borrower refuses to cooperate, you might need to hire a professional repossession agency.

- Store the vehicle: Once repossessed, you’ll need to store the car in a secure location.

- Sell or dispose of the vehicle: You can sell the car to recover some of the loan amount or dispose of it according to state law.

Seeking legal counsel throughout this process is highly recommended.

How to Remove a Primary Borrower from an Auto Loan

Removing the primary borrower from an auto loan can be a complex process, but it’s possible under certain circumstances.

Refinancing: The Most Common Solution

Refinancing the car loan in your name alone is often the most straightforward way to remove the original borrower. However, you’ll need to meet the lender’s credit and income requirements to qualify for refinancing. Additionally, if you’re considering adding a co-signer to improve your chances, the lender will assess the co-signer’s creditworthiness as a critical part of the refinancing approval process.

Alternative Options

- Loan assumption: In some cases, you might be able to assume the loan, becoming the sole borrower responsible for the debt.

- Selling the vehicle: If you can sell the car for a price that covers the remaining loan balance, you can pay off the debt and remove the original borrower.

Seeking Professional Help

Consult a bankruptcy attorney to understand your options if the borrower defaults. They can provide guidance on managing your financial obligations and handling the legal complexities of cosigning in California.

Legal and Financial Options for Cosigners

Filing for Bankruptcy

Filing for bankruptcy might be necessary if you face overwhelming debt due to the borrower not paying. Bankruptcy can offer relief and protection under California law, helping you manage unpaid debt and protect your financial health. Additionally, filing for bankruptcy can be a strategic move to manage unsecured debt, such as credit card debt, providing a pathway to financial recovery.

Debt Settlement Negotiations

Negotiating a debt settlement with the lender can reduce the overall amount owed and avoid further damage to your credit history. This process involves negotiating a lump sum payment that is less than the total debt.

Using a Debt Management Plan

Enrolling in a debt management plan can help manage credit card debt and personal loans, ensuring timely payments and reducing financial stress. These plans often involve working with a credit counseling agency to create a manageable repayment schedule.

Preventive Measures and Best Practices

Alternatives to Cosigning

Instead of cosigning, consider providing a lump sum to the borrower or helping them improve their credit score to qualify for a loan independently. Engaging in financial planning is another effective strategy that can help the potential borrower enhance their financial situation, potentially eliminating the need for a co-signer. This can reduce your risk and protect your financial health.

Creating a Legal Agreement with the Borrower

Drafting a private legal agreement with the borrower can outline their responsibilities and your rights as a cosigner. This agreement should include clauses that protect you if the borrower defaults.

Staying Informed About the Loan Status

Set up alerts and reminders to stay informed about the loan status and ensure the borrower makes on-time payments. Regularly checking the monthly statements can help you catch any issues early and take corrective action.

FAQs: Co-Signed Debt Lawyers Answer Your Burning Questions

Is a co-signer legally responsible for the loan amount if the borrower misses payments or defaults?

Yes, as a co-signer, you are equally responsible for the entire loan amount. If the borrower defaults, the lender can hold you liable for the remaining balance, including interest and fees.

What are the legal implications and cosigner rights in California if you co-signed a loan and the other party defaulted?

In California, co-signers have rights and responsibilities under both federal and state laws, including specific protections under consumer rights laws. If the borrower defaults, the lender can take legal action against both the borrower and the co-signer. This could involve collection efforts, lawsuits, or even wage garnishment.

As a co-signer, you also have the right to:

- Be informed: The lender must notify you if the borrower misses a payment or defaults on the loan, ensuring your consumer rights are respected.

- Request information: You can request information about the loan balance and payment history from the lender, a right protected under consumer rights laws.

- Seek legal counsel: Consult an attorney to understand your rights and options in case of default, including those related to consumer rights.

What should I do if I co-signed a loan for someone and they are now making late payments?

If the borrower is making late payments, act quickly to protect yourself:

- Communicate with the borrower: Discuss the situation and try to understand why they’re struggling to make payments. Offer support and solutions, if possible.

- Make the payments yourself: If you can afford it, making the payments temporarily can prevent damage to your credit score and avoid default.

- Consider refinancing: If the borrower’s financial situation is unlikely to improve, explore refinancing the loan to remove yourself as a co-signer.

- Seek legal advice: Consult a bankruptcy attorney to discuss your options and protect your legal rights.

Can I refinance the loan as the only option to remove the original borrower if they are not making payments on time?

Yes, refinancing the loan in your name alone is a potential solution. However, you’ll need to meet the lender’s credit and income requirements to qualify. Refinancing can remove the original borrower from the loan and protect your credit, but it might come with a higher interest rate or additional fees.

What are my rights as a co-signer if the borrower defaults on the loan, and can I sue them in small claims court to recover court costs and the loan amount?

As a co-signer, if the borrower defaults, you can:

- Pay off the debt: This will prevent further damage to your credit and stop collection efforts against you.

- Sue the borrower: You can take legal action against the borrower in small claims court to recover the money you paid, including any court costs and attorney fees.

- Negotiate a settlement: Try to reach an agreement with the borrower outside of court to repay the debt.

- Seek legal counsel: A bankruptcy attorney can advise you on the best course of action based on your specific circumstances.

Can I remove myself as a cosigner?

Some loans offer a cosigner release clause that allows you to be removed after a certain period of on-time payments by the primary borrower.

Don’t Face Co-Signer Stress Alone – Get Expert Help

Dealing with the fallout of a co-signed loan can be overwhelming. If you’re facing financial hardship or legal challenges due to a co-signed loan, seeking legal guidance is crucial. A bankruptcy attorney can:

- Assess your situation: Evaluate your financial situation and legal options.

- Negotiate with lenders: Communicate with lenders on your behalf to explore potential solutions.

- Protect your rights: Advocate for your interests and ensure you’re treated fairly.

- Explore bankruptcy options: If necessary, guide you through the bankruptcy process to obtain debt relief.

- Provide peace of mind: Having an expert on your side can alleviate stress and uncertainty.

At Kostopoulos Bankruptcy Law, we specialize in helping clients handle complex debt-related issues. Our experienced attorneys can provide the legal support you need to understand your rights, explore your options, and make informed decisions. Contact us today for a free consultation to discuss your specific situation.

Conclusion

Co-signing a loan is a significant decision with potential long-term consequences. Before you agree to co-sign, carefully weigh the risks and benefits, and ensure you understand your legal obligations. If you’re already facing challenges due to a co-signed loan, remember that you have options. Seeking legal counsel can help you understand the complexities and protect your financial future.

Disclaimer: This article provides general information and is not intended as legal advice. Consult with a qualified attorney for guidance on your specific situation.